|

|

|

Welcome to the Innovator

Welcome to the October 2020 issue of The Innovator, a monthly newsletter for iiM, LLC. What is iiM? We are a funding platform for early-stage companies in the animal health, agriculture and human health verticals. In this newsletter, we intend to share educational information, ideas and a perspective on the investments we are making. If you do not want to receive this publication, please let us know and we’ll remove you from the list of recipients. Please enjoy this issue of The Innovator.

Lydia Kinkade, iiM Managing Director

|

|

|

Entrepreneurship Capitalism Wealth Capitalism Wealth

By Philip Krause, iiM Counsel

I am privileged from time to time to guest lecture to a class at the University of Missouri—Kansas City’s School of Law or its Institute for Entrepreneurship and Innovation at the Henry W. Bloch School of Management. I also teach a law school class on the “Legal Life-Cycle of a High-Growth Technology and Life Sciences Venture.” My students are uniformly bright, inquisitive and well-studied, and derive from a wide cross-section of this country’s melting pot. They are “millennials” of course, and have a tendency toward concepts like wanting “social purpose” from their employers and jobs.

Here is a foundational point I nearly always make to my classes: entrepreneurship exploits and thrives on capitalism, which has as its primary purpose of creating wealth. Unless a start-up company has this primary purpose, it is likely to eventually fail, and moreover it is unlikely to attract investment capital.

|

Surprisingly, after centuries of creating an economic system that makes this country the envy of the world, this seemingly simple fundamental point is now being re-litigated. Perhaps the best example of the counter-argument is the “Statement on the Purpose of a Corporation” initially released by the Business Roundtable in August 2019. This statement, signed by a wide range of CEO’s representing some of the world’s largest corporations, lists no less than five fundamental corporate purposes, and does not presume to mention profits until its last stated purpose, “Generating long-term value for shareholders, who provide the capital that allows companies to invest, grow and innovate.”

Lest the sheer weight of signatories suggest a debate already concluded, today’s edition of The Wall Street Journal publishes the opinion piece of Andy Kessler, “To Serve the Public, Seek Profits.” Mr. Kessler begins with a quote from a current candidate for the U.S. presidency, “It’s way past time we put an end to the era of shareholder capitalism. Companies have responsibility to their workers, their community, to their country.” Mr. Kessler responds with several key points:

- Capitalism and competition create wealth; other systems slop existing wealth around.

- Profits aren’t greedy. They are a critical price signal—a measure of how well a company is deploying capital and creating value for society.

- Capitalism works by creating wealth. Equality comes best through the creation of ever-cheaper goods and services, not handouts.

Mr. Kessler cites Yale Prof. William Nordhaus, winner of the 2018 Nobel Prize in Economics, “Only a minuscule fraction of the social returns from technological advances over the 1948-2001 period was captured by producers, indicating that most of the benefits of technological change are passed on to consumers.” Prof. Nordhaus has quantified this return as follows, “Innovators were able to capture about 4 percent of the total social surplus from innovation.” According to Mr. Kessler, this “social surplus” creates “the improvements capitalism brings to common living standards. That is societal wealth.” In short, when a business focuses on creating wealth, the happy by product is more affordable goods and services, and the opportunity for shareholders to engage their own charitable purposes. Hence, the betterment of society is the natural outcome of a well-executed enterprise purposed to create wealth for its owners.

|

The venerable Prof. Milton Friedman, winner of the 1976 Noble Prize in Economics, described as “the most influential economist of the second half of the 20th century . . . possibly of all of it” (The Economist, Nov. 23, 2006), explained these principles in his article, “The Social Responsibility of Business is to Increase its Profits” (The New York Times Magazine, Sept. 13, 1970). Prof. Friedman argues that managers who claim their business is concerned primarily with whatever may be the contemporary favored social purposes “are unwitting puppets of the intellectual forces that have been undermining the basis of a free trade society. . .” Instead, Prof. Friedman’s article concludes, “there is one and only one social responsibility of business—to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game, which is to say, engages in open and free competition without deception or fraud.” (Emphasis added.)

Entrepreneurs who would pursue their inventive impulses using others’ capital, and lawyers who would advise them, do well to keep these foundational principles in focus. As a practical matter, capitalism can be a ruthless taskmaster, squeezing every possible efficiency from a venture, forcing a laser focus on its business plan. If the entrepreneur gazes elsewhere, the competitors will pass by in the fast lane.

Likewise, investors demand returns on their capital investment and will hold management accountable to their promises. When management diverts attention and resources to non-productive or collateral purposes, the underlying rationale for investing in the company is diluted or undermined, and investors will become intolerant of the folly.

This is not to suggest that Aristotle’s ancient teachings on persuasion derived from personal character are rendered irrelevant, i.e. this is not a rationale for corrupt practices, nor that the ends justifies the means. Effective execution of a business plan may very well require good wages and benefits to attract the best talent. Or, polluting the nearby stream might result in business-destroying penalties, so that clean operations are more likely to lead to profits. As Prof. Friedman concludes, a business has a duty to operate within the rules of the game, through open and free competition.

Yet, as much as some would seek to discredit the notion, the robust bottom line is indeed the scorecard of success. Not simply to satisfy a craving for materiality, but because that is the means by which society has an opportunity to be made better for all. Seemingly oxymoronic, a business that primarily emphasizes social purpose is less likely to achieve either profits or social purpose, while a business that primarily focuses on profitability is more likely to achieve both.

|

|

|

Venture Investing Terminology

There are many terms in the venture capital world that can be confusing. As we look at various companies and meet with their founders, you may hear us use some of this terminology. Here are a few such terms and what they mean.

Conversion Rate or Ratio – Means the number of shares of Common Stock into which each share of Preferred Stock is convertible.

Lead Investor – The investor who takes on most of the work in negotiating the investment terms, doing due diligence, and monitoring the company after the closing. The lead investor usually invests more than other investors who participate in the round. The lead investor is often located near the company or specializes in the company’s industry.

Most Favored Nation – A most favored nation clause, referred to as a MFN clause, is an unusual convertible note term that allows the convertible note holder to elect to inherit any more favorable terms that are offered to any subsequent investors following the original investor's investment and prior to a next equity round.

Revenue Run Rate – The Revenue Run Rate (also run rate — one word) is the annualized revenue of a company if you were to extrapolate the current revenue over a year. It refers to the financial performance of a company based on using current financial information as a predictor of future performance. The run rate functions as an extrapolation of current financial performance and is based on the assumption that current conditions will continue. Run rates are useful for new business or business units within a company that have only had a short period of revenue generation opportunity. This figure allows managers, venture capitalists and investors to measure the annualized revenue.

|

|

|

Angel Investing Exits: The Good, the Bad and the Ugly

By Hambleton Lord & Christopher Mirabile

Seraf Co-Founders

Having spent the past 15 years as an active angel investor in Boston, managing a large angel group, and keeping up-to-date with angel activities around the US, Ham has a great perch from which to develop a perspective on what it takes to go from investment to exit.After a year or two down the path of building a diversified portfolio of angel investments, many individual angels are faced with some uncertainty about their path forward. The questions on many experienced angels’ minds are “Will I make a good enough return on my angel investments to justify the risk? Should I continue to invest?”

Q: At Launchpad, we worked on a research project to understand the different kinds of exits we had in our portfolio. Give us a summary on the research methodology and findings?

At the time of our research project in the Fall of 2012, we had 17 exits in our angel group (it’s now about 24 exits). About half the exits were positive exits and the other half each returned less than we originally invested. The sample size we examined was large enough to gather some interesting insights. We looked at each company and recorded the following data:

- Time from initial investment to exit

- Total number of rounds of investment

- Types of investors (e.g. Angels, VCs, Corporate Investors, Friends & Family)

- And finally, the amount of capital returned to investors

|

The chart on the right provides a visual explanation of what exits look like in the context of startup companies. We think this chart gives a great overview of what angel investors can and should expect within their angel investment portfolio. So let’s walk through this chart in more detail. The arrows that point down represent the different ways companies fail and return less than the capital originally invested. These companies may return some capital, but for you the angel investor, you will see little return.

Fail Fast on Seed Only: If you are doing a good job finding companies, performing due diligence, and sizing the initial rounds to get to key milestones, there should be a limited number of companies in your portfolio that fail quickly. In our portfolio, these companies were usually characterized as early seed deals where a great idea didn’t pan out. The company raised a small amount of capital, but the technology didn’t work, or customers weren’t interested in buying for any one of a whole host of reasons. As seed investors, you decide to stop funding the company and the company can’t find any other investors. Although losing all your money in a seed deal doesn’t feel great, typically you put a small amount of money into the company at this stage. So your overall loss in time and money tends to be low. Remember, the only thing worse than a mistake, is an expensive mistake. A typical Fast Fail scenario has less than $1M invested in the company, and it took less than 18 months to fail.

|

Fail After Multiple Angel Rounds: This is probably the most common scenario for failed angel deals. You find a great team with an awesome product. The company makes some early progress, but not enough to raise a large follow-on round of financing. So you and your angel colleagues pony up a bridge round to help the company achieve the milestones that the big investors need to see. One bridge round turns into two or three bridge rounds, with the plausibility of each successive round buttressed by the human tendency to not want to admit you were wrong until you are absolutely forced to. So you chip into the pot to see the next card. Before you know it, you’ve invested 2x or 3x what you put into the first round, and it’s four years after you made your initial investment. And, the company continues to underachieve. At this point, the old investors are ready to bail, and new investors aren’t interested. So, if you are lucky, you unload the company at a fire sale price to some other company. In the end, you lost much, if not all, of your investment and you spent 4 years going through this exercise. A typical scenario in this situation has $1M to $3M invested in the company over a 3 to 5 year time frame.

Fail After Angel and VC Rounds: Some of the most promising startups end up in this bucket. The story goes something like this… you invest in the seed round, the company gets some early traction and shows good signs of product/market fit. Times are buoyant, competition for good deals is hot so VCs start to take interest and the company closes a Series A round of financing at a nice step up in valuation. On paper, your seed investment is now worth 3x what you invested. Things are looking good! Unfortunately, the initial success doesn’t pan out and growth stalls at the company. But, no one is willing to call it quits, so the VCs force a pivot or maybe some change to management and the company raises additional rounds of financing. Your initial stake in the company keeps getting diluted unless you pony up with additional funds at increasing valuations. In the end, the company gets sold or shut down and your return is zero. A typical scenario in this situation has $10M to $20M invested in the company over a 7 to 10 year time frame.

Zombie - Cash Flow Positive, but Slow Growth - No Liquidity: We’ve We've all invested in companies like this. The business grows slowly but surely. Revenues climb into the millions and the company can easily stay around cash flow break-even because it is only making modest investments in growth. However, the growth rate for the business is in the low single digits, the company cannot attract a big slug of capital to force growth, and the company remains below the radar of any potential buyer. This situation is relatively common with angel backed companies and less so with VC backed companies. The main reason for this is that VCs have to distribute the assets of their fund to their investors around the 10 to 13 year mark. Having to distribute stock in a private company is not ideal. So many VCs will force the sale of a zombie-like company. Angels are less motivated to force the sale of a company, so they end up holding their investment for much longer than they ever expected. Many zombies are just lifestyle companies in disguise. The founding team has no motivation to sell because there are no interesting offers, they are drawing a nice salary and aren’t working as hard as they did in the early startup days. If you are an investor in a company that fits this description, get together with the other investors and work with the CEO to come up with an exit plan.

So we reviewed the not so good exits, but what about the positive exits? This is the fun and lucrative part of angel investing. What do those exits look like? Stay tuned for Part 2 of this article where we will review everything from an early exit to an IPO.

|

|

|

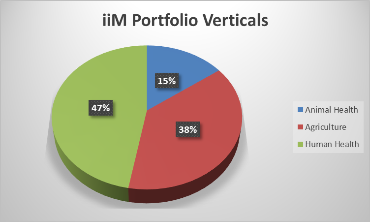

A Look at the iiM Portfolio

iiM (Innovation in Motion) is a funding platform for early stage companies in the Animal Health, Human Health and Agriculture verticals. The company invests $100,000 - $500,000 in selected companies. iiM is building a diversified portfolio of companies – currently there are 11 with commitments to fund at least three more – with a target of at least 30 to 40 portfolio companies across the United States and Canada. We typically invest in companies at Seed or Series A stage and have made a total investment in these companies (including the three commitments) of slightly more than $3.1 million. To date, we have also made five follow-on investments in portfolio companies.

We are unlike most other angel groups in that we specialize in only three industry verticals and have deep domain expertise within our investment group that is called upon to evaluate the companies we consider. It is also notable that we have a professional team that sources companies and performs extensive due diligence.

iiM has an investor group that serves as an investment committee as well as a syndicate that invests alongside the investor group. The iiM Syndicate entitles its members to participate in all the iiM meetings and pipeline calls; review prospective investments; view due diligence materials and invest only in those companies that each member chooses. And, an investment can be as little as $5,000.

Why a syndicate? Syndicate members invest alongside iiM Investor Members to produce a cumulative capital investment that is meaningful to new portfolio companies. Further, if the capital commitment is large enough, iiM may be in a position to lead the investment round and secure even better terms and conditions for all investors. In one investment, Investor and Syndicate members pooled capital totaling $530,000 to invest in a Series A Preferred Stock round. Syndicate members must be Accredited Investors and pay $2,500 per year to participate.

If you are interested in attending an iiM meeting or want more information about the iiM Syndicate, please contact Lydia Kinkade, Managing Director, at lkinkade@iimkc.com or (913) 671-3325. The iiM website is www.iimkc.com.

www.iimkc.com

|

|

|

| |

|

| |

|

|